If you’ve ever faced a vet bill that made your jaw drop, you’re not alone. Emergency care, surgeries, or even chronic conditions can rack up costs quickly, and that’s where pet insurance comes in. But if you’ve never used it before, it can feel a little confusing. Is it like human health insurance? Do you pay the vet directly or get reimbursed later? And most importantly—does it actually save you money in the long run?

Let’s break it all down in plain English so you know exactly how pet insurance works (and whether it’s worth it for your furry family member).

What Pet Insurance Actually Covers

The first thing to know is that pet insurance is designed to help with unexpected vet expenses. Think broken bones, swallowed socks, or sudden illnesses. Most policies do not cover routine or preventive care unless you add it on.

Here are the main categories of coverage you’ll see:

-

Accident-Only Plans: These cover injuries like fractures, cuts, or poisoning. Good for “just in case” situations, but won’t help with illness.

-

Accident + Illness Plans: The most common type, covering things like cancer, ear infections, diabetes, and more.

-

Wellness Add-Ons: Optional coverage for routine stuff—vaccines, flea prevention, dental cleanings, etc.

Example: If your dog tears her ACL, an accident + illness plan could cover surgery costs. But her annual exam or rabies shot would only be covered if you opted into a wellness package. Companies like Embrace Pet Insurance offer this type of flexibility—you can choose core illness/accident coverage and then add on wellness care if you want the routine stuff included.

Highly customizable plans that let you fine-tune your premium while keeping strong overall coverage.

How the Payment Process Works

This is where pet insurance is different from human insurance. With most plans, you’ll pay the vet bill upfront and then submit a claim for reimbursement.

Here’s the usual process:

-

Your pet sees the vet.

-

You pay the full bill.

-

You submit a claim online (usually by uploading your invoice).

-

The insurance company processes it and reimburses you via direct deposit or check.

Some companies now work with vets directly, so you only pay your portion while insurance pays the rest behind the scenes—but that’s still less common.

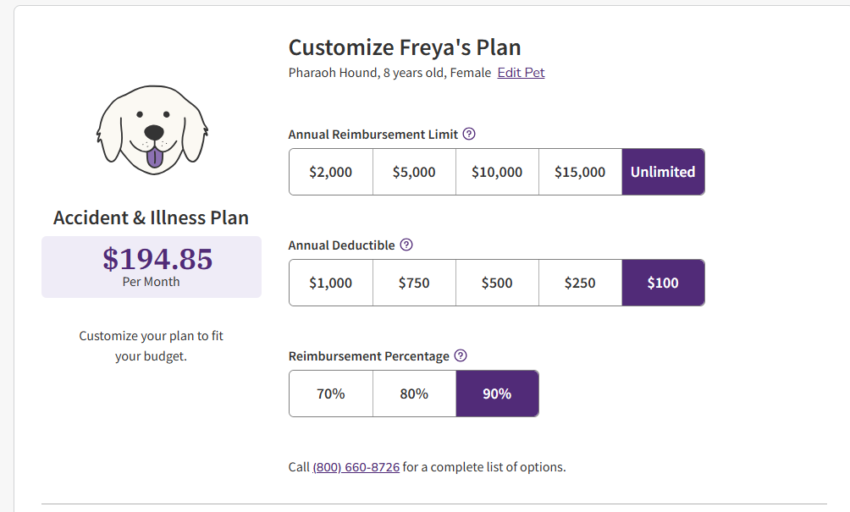

Key Terms You’ll See Everywhere

Pet insurance has its own lingo, and understanding it helps you make sense of the numbers.

-

Premium: What you pay each month or year for coverage.

-

Deductible: How much you have to pay out of pocket before insurance kicks in.

-

Reimbursement Rate: The percentage the company pays after you hit your deductible (often 70%, 80%, or 90%).

-

Annual Limit: The max amount your insurance will pay in a year. Some have no limit, which is great if your pet develops something serious.

Example: Let’s say your cat needs a $2,000 surgery. If you have a $250 deductible and 80% reimbursement with a $10,000 annual limit, here’s what happens:

-

You pay the first $250 (deductible).

-

Of the remaining $1,750, insurance reimburses 80% ($1,400).

-

You’re left paying $600 total instead of the full $2,000.

Pre-Existing Conditions—The Big Caveat

Almost all pet insurance companies do not cover pre-existing conditions. That means if your dog has already been diagnosed with allergies or your cat has kidney disease, those won’t be reimbursed.

This is why it’s best to get insurance when your pet is young and healthy. The younger they are, the fewer pre-existing conditions to worry about, and the lower your premium usually is.

Customizing Your Plan

Most pet insurance companies let you choose your deductible, reimbursement rate, and annual limit. A higher deductible usually means a lower premium, and vice versa.

For example, you might choose:

-

A $200 deductible with 90% reimbursement (higher monthly cost, but less out of pocket at the vet), or

-

A $500 deductible with 70% reimbursement (lower monthly cost, but you’ll pay more if something happens).

It really depends on how much risk you’re comfortable with and your monthly budget.

Why Pet Insurance Can Be Worth It

At first glance, paying $30–$70 a month might feel like “just another bill.” But one unexpected emergency can wipe out years of savings.

A few real-world examples:

-

Foreign object ingestion (hello, sock-eating dogs): $1,500–$3,000

-

Hip surgery: $4,000–$6,000

-

Cancer treatment: $5,000–$10,000+

Pet insurance gives you peace of mind that you won’t have to choose between your pet’s health and your bank account.

Pet Insurance FAQs

Does pet insurance cover dental care?

It depends. Most plans will cover dental injuries (like if your dog breaks a tooth in an accident), but not routine cleanings. Some insurers, including Embrace, offer optional wellness add-ons that can help with dental cleanings and preventive care.

Can I use any vet, or do I have to stay “in-network”?

One of the perks of pet insurance compared to human insurance is freedom—you can typically go to any licensed vet, emergency clinic, or specialist in the U.S. That means you don’t have to stress about staying “in-network.”

Do premiums go up as my pet gets older?

Yes. Just like with human health insurance, your monthly premium usually increases over time because older pets are more likely to need care. That’s why starting when they’re young often saves money long-term.

Are hereditary conditions covered?

Many insurers do cover hereditary and congenital conditions (like hip dysplasia or heart disease), as long as they weren’t diagnosed before you signed up. Always read the fine print so you know exactly what’s included.

Does pet insurance pay the vet directly?

Most of the time, no—you’ll pay the bill first and get reimbursed. That said, a few insurers are starting to offer direct-pay options at certain clinics, so it’s worth asking your vet if they partner with any companies.

Can I have more than one pet on the same policy?

Not usually. Each pet typically needs their own plan, but some companies give you a multi-pet discount if you enroll more than one.

How quickly do claims get reimbursed?

It varies by company. Some process claims in just a few days (especially if you submit them online), while others can take a couple of weeks. Choosing an insurer with a good track record here can make a big difference in peace of mind.

Final Thoughts

So, how does pet insurance work? In a nutshell: you pay a monthly premium, and in exchange, you’re covered (or reimbursed) for unexpected vet bills—minus your deductible and copay. It’s not perfect, and it won’t magically make vet care free, but it will protect you from those “oh no” moments that could otherwise leave you scrambling.

If you’re on the fence, think about your pet’s breed (some are prone to health issues), your budget, and how much peace of mind is worth to you. At the end of the day, pet insurance is about making sure you can say “yes” to the best care when your furry friend needs it most.

-3")